Greetings to everyone who’s already dived into the first part of our gripping chronicle of the events that shaped Bitcoin’s history. It's time to move forward and explore the next chapter of developments and technologies that paved the way for the evolution of the world’s first cryptocurrency, ultimately bringing us to where we are today.

Mining and Early Adoption

Bitcoin, as a digital currency, operates through a process called mining. Imagine a bunch of computers racing against each other to solve a complex puzzle, whoever cracks it first gets rewarded in shiny new bitcoins.

Can you even imagine that back in the day, you could mine crypto using just your trusty old home PC? No need to splurge on pricey mining rigs; it was as simple as turning on your computer and keeping a steady internet connection.

It’s hard to believe that there was once a time when you could mine 1 Bitcoin a day with just a home PC, but that was the reality back then.

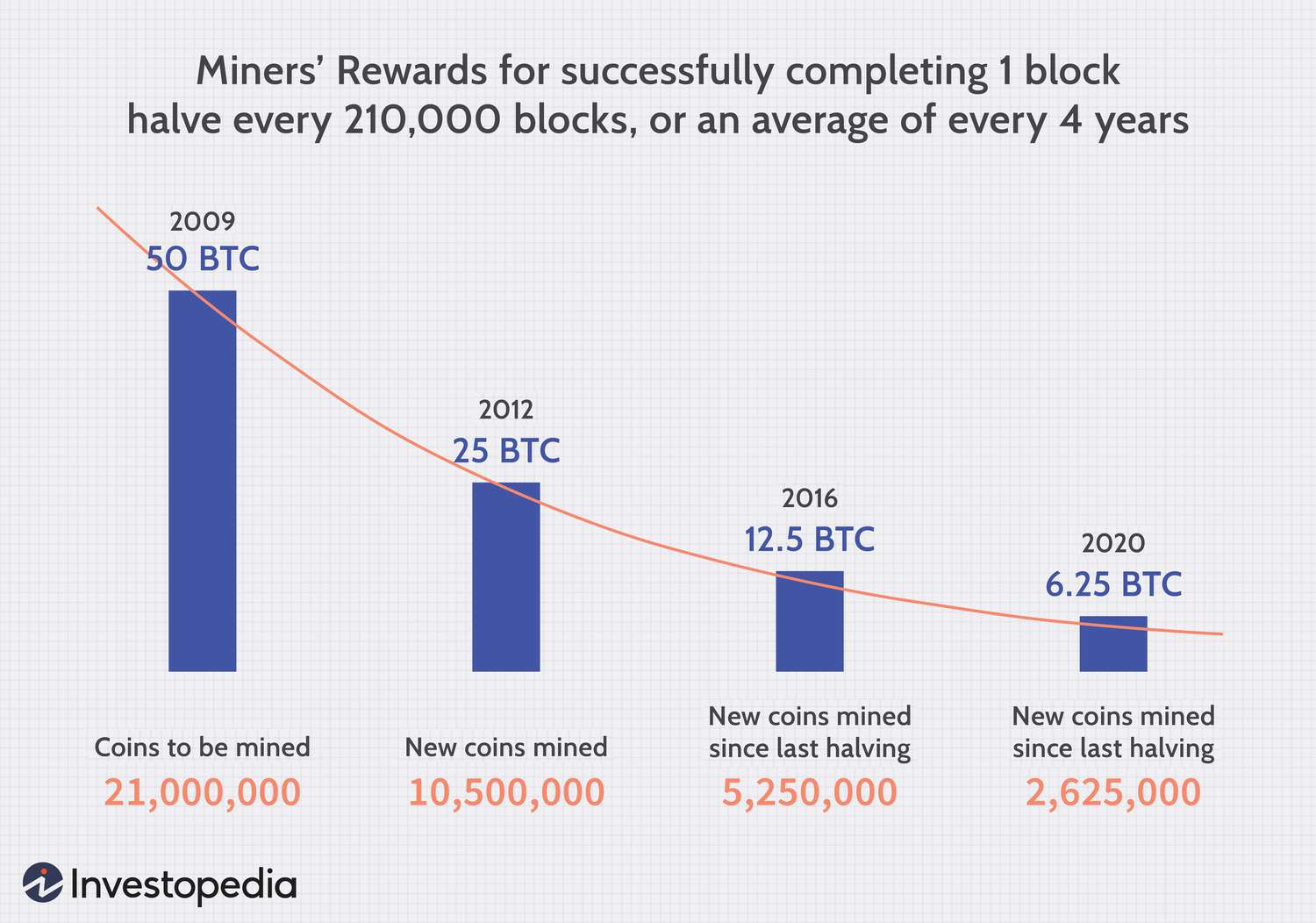

Mining Bitcoin today is no longer a simple task you can do with just a regular computer.

Now, it takes serious hardware and a lot of resources:

- First, you need powerful, specialized devices ASIC miners. These gadgets can perform massive amounts of calculations way faster than your average PC.

- Second, mining consumes a lot of electricity. So, the best place to mine Bitcoin is where the electricity is cheap — because, let's face it, your electric bill will be through the roof otherwise.

- And third, you need a reliable internet connection and proper cooling. ASIC miners get hot, really hot, so keeping them cool is essential if you want them to run smoothly without catching fire.

Under current conditions, it would take about two years to mine one bitcoin on an ASIC miner, even if you're part of a large mining pool. Alone it would take way longer and might even end up costing more in hardware and electricity than the actual Bitcoin you’d eventually mine.

The Rise of Mining Pools

Bitcoin mining gets trickier every year, which is why miners have started to team up in what we call mining pools. These are groups of miners who combine their computational power to solve problems together. When the pool cracks the correct hash, the reward is shared among members based on their contribution.

To put it in perspective, let’s do some real-world math. On average, it takes the entire network about 10 minutes to find one block, and the reward is split among all the miners.

Now, if you’re using the latest Antminer S19 Pro+, with the current difficulty and hash rate, your chance of finding a block solo is a tiny 0.0000003%. So, mining Bitcoin on your own not really worth it. That’s why miners join pools — share the load, share the reward.

The network’s difficulty and competition have gotten so intense that mining solo is almost impossible. The odds of finding a block are so small it would take an eternity (or so it feels).

Pools boost your chances of earning a reward and give you more predictable income, even though it’s smaller than if you mined alone. For example, mining in a pool with with the same Antminer S19 Pro+ could bring in about 0.0015 BTC a day, or 1 Bitcoin in roughly two years.

The First Mining Pools

Slush Pool was one of the pioneers in bringing the idea of collaborative mining to life, making mining both accessible and profitable again for individual miners. Founded in December 2010 by Marek Palatinus, widely known in the community as Slush, this pool was the world’s first publicly available mining pool — and its Bitcoin cultural impact was immediate.

Before mining pools, the mining rewards were significantly higher, but so were the risks and computing power requirements. Slush Pool Bitcoin revolutionized the process by offering a fair and transparent system for distributing rewards based on a miner’s contribution to the pool.

What made it so innovative? Well, Slush’s Pool was one of the first to introduce a hash rate evaluation system, ensuring that rewards were distributed fairly. It also offered detailed, real-time stats for miners to track their performance, along with robust security features to protect against potential threats.

Laszlo Hanyecz’s purchase of two pizzas for 10,000 BTC

Every year, starting from May 22, 2010, the crypto community celebrates this day to reflect on how far the technology has come and how Bitcoin, even among all the new cryptocurrencies, has stood the test of time.

Laszlo Hanyecz Bitcoin Pizza Day isn’t just a celebration for pizza and crypto lovers—it’s the story of the first-ever commercial transaction using Bitcoin to buy two large pizzas from Papa John’s.

Thank You Laszlo, and Happy #Bitcoin Pizza Day. pic.twitter.com/z5cl46DZsq

— Michael Saylor⚡️ (@saylor) May 22, 2024

Hanyecz, one of the early Bitcoin miners, has already mining crypto on his computer since 2009. As a pizza fan, he had an idea: why not see how practical and useful Bitcoin could be by using it to buy a pizza?

Happy #Bitcoin Pizza Day 🍕 pic.twitter.com/Pz0MW7ZO1Y

— Lina Seiche (@LinaSeiche) May 22, 2024

Back in 2010, Hanyecz’s pizza purchase was seen as a quirky experiment by forum users, but since then, it has taken on much greater significance. Over the years, Bitcoin Pizza Day significance has become the major cryptocurrency milestone of the early days of Bitcoin history — a reminder of how far the first digital coin has come in the past decade.

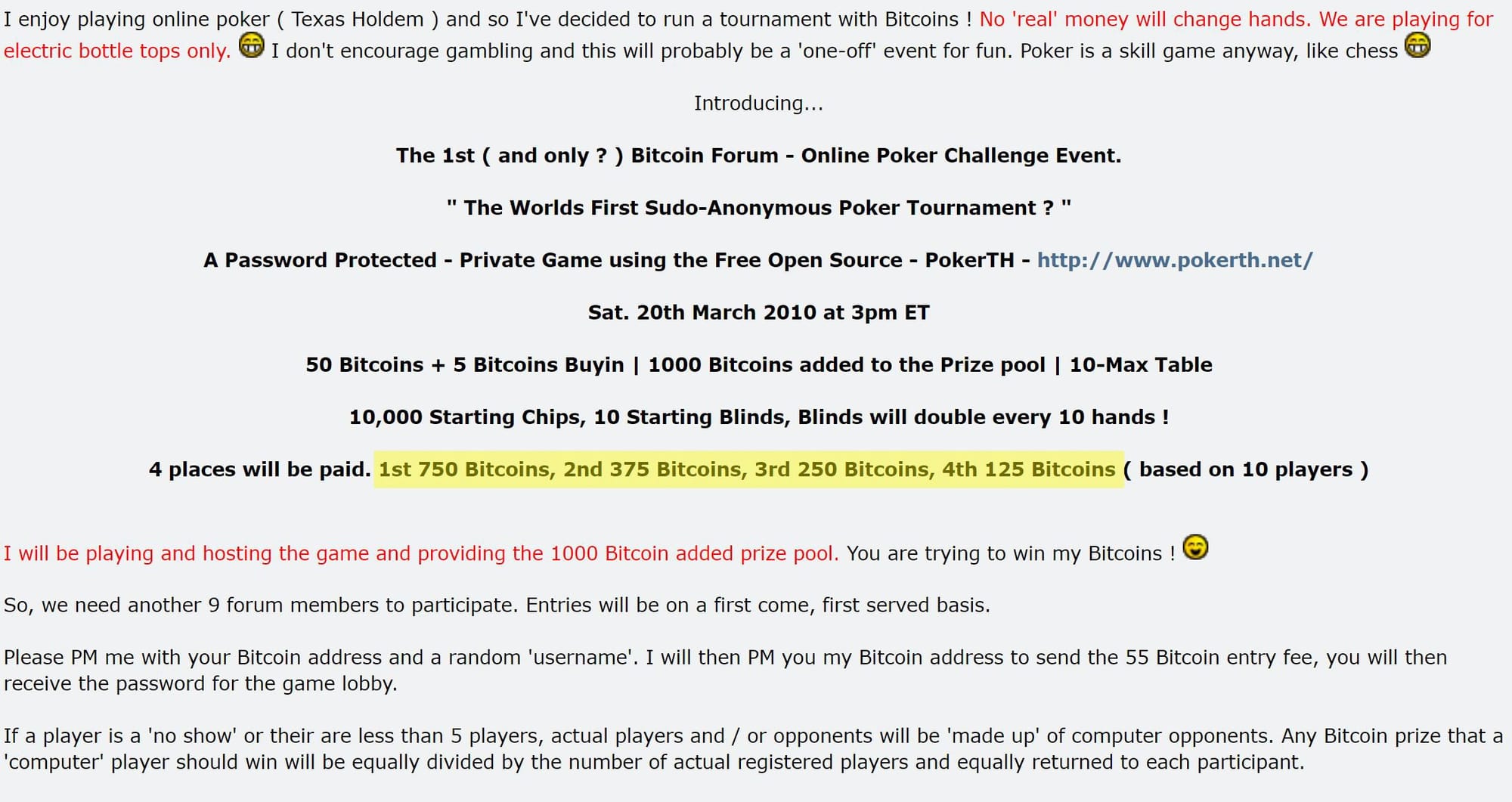

The 1,000 BTC Poker Game

In addition to buying pizza, Bitcoin was already catching the eye of professional poker players and gambling enthusiasts in the early 2010s. Using Bitcoin for betting offered a chance for participants to stay anonymous and sidestep the financial limitations that came with traditional platforms.

As Bitcoin started to gain traction, many professional players turned to it for online gaming, just ahead of the first major price boom at the end of 2013. Ed Moncada, a former poker pro and co-founder of Blockfolio, was one of the first to hop on board.

He told Cointelegraph Magazine:

There are some high-stakes players who are pretty well-known in the Bitcoin world. I know poker players who are holding Bitcoins worth millions.

Bryan Micon, the promoter of Seals With Clubs, the first Bitcoin poker game site in the U.S., says there were plenty of players who made more money from Bitcoin than they ever did from poker.

In the early days, there were 1000-coin pots, and those who decided to cash out and hold onto them changed their entire lives.

The WikiLeaks Bitcoin Donations Controversy

After the release of sensitive military information, PayPal, under growing pressure, froze the account of the fund linked to WikiLeaks, stating that "PayPal cannot be used for any activity that promotes, facilitates, or instructs others to engage in illegal activity."

Meanwhile, U.S. officials were working hard to crush any support for the organization. Senator Joe Lieberman personally reached out to Tableau Software, pushing them to stop supporting WikiLeaks’ visualizations. The Swiss bank PostFinance froze the personal account of Julian Assange, and MasterCard and Visa refused to process any further transactions for WikiLeaks.

Unable to collect and store funds by other means, WikiLeaks turned to Bitcoin donations. They set up a payment channel in June 2011. This came after the price had surged, and a Bitcoin community growth of miners and users had formed, but not before political pressure — already squeezing major financial institutions into submission — could be applied to the fledgling Bitcoin community. According to Julian Assange, WikiLeaks received Bitcoin after what he described as the "illegal U.S. financial blockade."

WikiLeaks now accepts anonymous Bitcoin donations on 1HB5XMLmzFVj8ALj6mfBsbifRoD4miY36v

— WikiLeaks (@wikileaks) June 14, 2011

Julian Assange later commented that he made a whopping 50,000% profit from Bitcoin as a direct result of the U.S. government’s financial blockade of WikiLeaks.

In one of his final posts, Bitcoin’s creator, Satoshi Nakamoto, warned WikiLeaks against using Bitcoin, fearing that the association might destroy his creation.

"It would be nice to attract attention in any other context. WikiLeaks stirred up a hornet’s nest, and the swarm is heading toward us," Satoshi added in his literal penultimate post on BitcoinTalk.

But despite Satoshi's warnings, the fact remains: Bitcoin and WikiLeaks saved each other. WikiLeaks saved the nascent Bitcoin community from excessive political pressure that its creator feared wouldn’t let it survive. In turn, Bitcoin saved WikiLeaks from financial ruin due to the U.S. financial blockade that was intended to crush it.

Growth of the First Bitcoin Communities

The domain name "bitcoin.org" was registered in 2008 by an anonymous entity using a privacy service to hide their identity. To this day, the person behind it remains a mystery, though many believe it was Satoshi Nakamoto, the pseudonymous creator(s) of Bitcoin.

The first creation was Bitcoin.org — an official site where the White Paper and source code were published. Today, the domain is maintained by a community of developers and volunteers working on the Bitcoin Core software and related projects. The site acts as a central hub for all things Bitcoin, including beginner guides, technical documentation, news, and ecosystem updates. It also provides resources for those new to the Bitcoin economy, with a starting point for buying Bitcoin and information on how to run Bitcoin nodes.

The Bitcointalk.org forum came later, in 2009, to support the growing community and help early users and developers exchange knowledge and experiences. The forum quickly became the go-to space for discussing the technical aspects of Bitcoin, mining, cryptography, and economics. Satoshi was an active participant, answering questions and sharing thoughts on Bitcoin's future. It was here that the first announcements of important updates were made.

In the early days, Bitcointalk saw some heated debates. Key topics included scalability, security, censorship resistance, and decentralization. It was on the forum that changes to the code, the addition of new features, and potential forks of the network were hashed out.

As interest in Bitcoin grew, local communities began to form, and offline meetups were organized. Initially, these gatherings were arranged through Bitcointalk forum and others, where participants would agree on the time and place to meet. These events gave users a chance to exchange experiences, discuss strategies, and make new connections.

The First Bitcoin Faucet

On June 12, 2010, was launched the first Bitcoin faucet by Gavin Andresen. A Bitcoin faucet is a website or app that gives away small amounts of Bitcoin to visitors in exchange for completing tasks listed on the site.

That same year, he gave away a staggering 19,700 bitcoins to users who did nothing more than solve a CAPTCHA. Initially, he was handing out five bitcoins per person. Rewards were distributed regularly for completing simple tasks or winning easy games.

The first bitcoin faucet was created by @gavinandresen and was giving out 5 BTC per claim. pic.twitter.com/f5WTKBDCGG

— Crypto฿ull (@CryptoBull) January 3, 2018

If Andresen had kept those coins, today they'd be worth around $1.5 billion. But unlike today's Bitcoin enthusiasts, Andresen was directly in touch with Satoshi Nakamoto and was a true believer in the vision of a global peer-to-peer electronic currency system.

So, how could Andresen give away so many bitcoins? Simple! The price was the least interesting thing about Bitcoin back then. Smart developers like Andresen were more focused on making Bitcoin useful as a currency, which is why they created tools like the Bitcoin faucet to generate new transactions.

The Bitcoin adoption history during this period reflects the unyielding belief in the potential of decentralized finances despite the lack of tangible value. Whether it was the symbolic Bitcoin Pizza Day or the rebellious donations to WikiLeaks, each chapter of Bitcoin’s early history reflects the profound influence it had on the broader societal norms. As we look back on these moments, it's clear that Bitcoin is a cultural revolution that continues its journey from an obscure digital concept to a globally recognized asset.

Disclaimer: All materials on this site are for informational purposes only. None of the material should be interpreted as investment advice. Please note that despite the nature of much of the material created and hosted on this website, HODL FM is not a financial reference resource and the opinions of authors and other contributors are their own and should not be taken as financial advice. If you require advice of this sort, HODL FM strongly recommends contacting a qualified industry professional.