Sam Bankman-Fried, the imprisoned founder of collapsed cryptocurrency exchange FTX, has once again stirred controversy after his long-dormant X account posted a 14-page document late Thursday night, claiming that FTX “was never insolvent.” The post, which appeared nearly three years after the exchange’s dramatic downfall and less than a year into his 25-year prison sentence, has reignited debate across crypto and legal circles about the true nature of FTX’s collapse.

A surprise post revives old arguments

The post shared from Bankman-Fried’s verified X account linked to a document titled “FTX: Where Did The Money Go?” The report, allegedly prepared by Bankman-Fried and his team, insists that the exchange’s implosion in November 2022 was caused not by fraud, as concluded by a Manhattan jury in 2023, but by a “liquidity crisis” that could have been resolved within weeks.

According to the document, FTX held $25 billion in assets and $16 billion in equity value against $13 billion in liabilities when bankruptcy proceedings began. It claims that “external counsel” intervened prematurely, forcing the company into Chapter 11 protection before it could recover. “FTX was never bankrupt, even when its lawyers placed it into bankruptcy,” the document argues.

The report asserts that, if managed differently, FTX’s asset portfolio, including large stakes in companies such as Anthropic ($14.3 billion), Robinhood ($7.6 billion), Ripple, SpaceX, and Genesis Digital Assets, would now be worth $136 billion.

SBF’s ongoing narrative of victimhood

The claims closely mirror Bankman-Fried’s previous public statements, including a March 2025 prison interview with Tucker Carlson, where he maintained that “there was enough money to pay everyone back.” The former FTX CEO continues to portray himself as the victim of political targeting and legal overreach rather than the orchestrator of one of cryptocurrency’s largest frauds.

In recent months, someone operating on behalf of Bankman-Fried also used social media platform GETTR to allege that his arrest was timed for political reasons, blaming his donations to both Democratic and Republican campaigns for his downfall. The new document extends those assertions, suggesting that regulatory and legal interference, not internal misconduct, caused the exchange’s demise.

Data points and contradictions

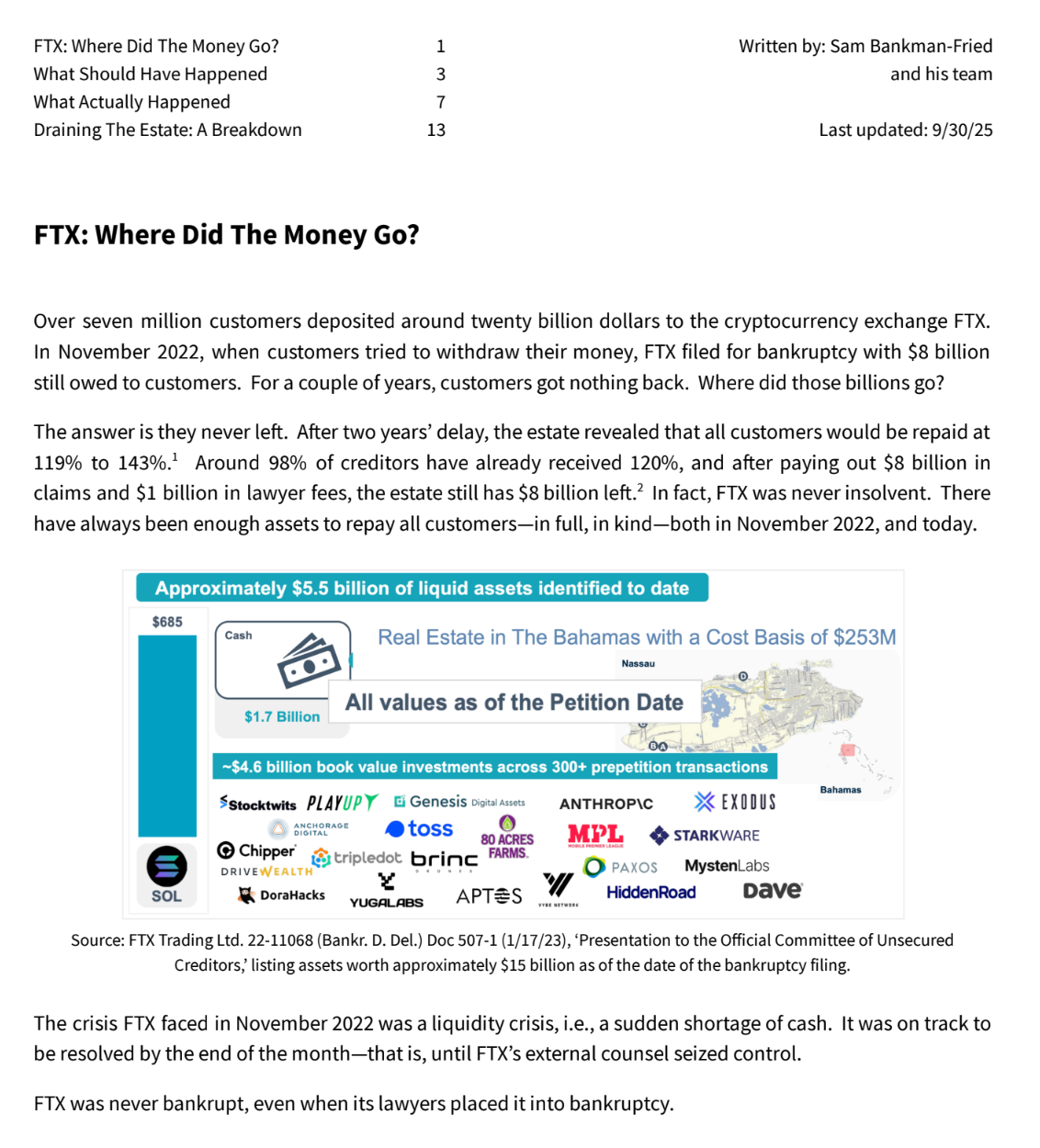

The 14-page memo highlights what it describes as FTX’s undervalued holdings in digital and traditional assets. Among those listed are 58 million SOL tokens, 205,000 BTC, and more than $1.7 billion in cash and stablecoins at the time of bankruptcy. It further notes that over seven million customers deposited approximately $20 billion on the platform.

The document points out that as of 2025, 98% of FTX’s creditors have received at least 120% of their claims, citing reports from the FTX estate’s ongoing recovery process. It also claims that, after repaying debts and legal fees reportedly totaling $9 billion, an additional $8 billion in residual assets remain.

However, critics have been quick to dismiss the latest defense. Legal experts and former creditors noted that these arguments echo positions Bankman-Fried’s lawyers raised during trial, all of which were rejected. Forensic audits presented in court found that billions in customer funds were diverted to FTX’s sister trading firm, Alameda Research, for high-risk ventures and personal expenses.

Community backlash and skepticism

The crypto community’s response was swift and scathing. Many industry figures said the new report was an attempt to rewrite history. Venture capitalist Adam Cochran summarized the prevailing sentiment bluntly on X: “Shut the (expletive) up, Sam. You stole.”

Shut the fuck up Sam.

— Adam Cochran (adamscochran.eth) (@adamscochran) October 31, 2025

You stole. https://t.co/IMbOpTzTn2

The document’s timing came just weeks after conservative activist Laura Loomer claimed there was a “well-funded” effort to lobby former U.S. President Donald Trump for a pardon on Bankman-Fried’s behalf, a claim that has not been substantiated.

You’re going to start seeing a lot more in the news about Sam Bankman-Fried.

— Laura Loomer (@LauraLoomer) October 14, 2025

There is a massive and well funded lobby effort to get this criminal pardoned. He’s going to pretend like he was a victim of Joe Biden and the Democrats after he funded all of the Left’s campaigns.… https://t.co/ai2zmWuFu0

The self-published report may rekindle interest in post-mortem analyses of FTX’s downfall, but experts caution that nothing in the new material changes the core legal outcomes. Bankman-Fried remains convicted on seven federal charges, including wire fraud and conspiracy, and is currently serving his sentence at a federal facility.

An unending saga

Despite being behind bars, Bankman-Fried continues to influence public discourse around his case through periodic statements and media proxies. The latest document underscores his determination to challenge the official record of FTX’s collapse.

Still, as former U.S. District Judge Lewis Kaplan, who sentenced Bankman-Fried in 2024, remarked at the time:

“A thief who takes his loot to Las Vegas and successfully bets the stolen money is not entitled to a discount on his sentence.”

For most observers, no 14-page manifesto, however data-packed or boldly worded, is likely to reverse that verdict.

Disclaimer: All materials on this site are for informational purposes only. None of the material should be interpreted as investment advice. Please note that despite the nature of much of the material created and hosted on this website, HODL FM is not a financial reference resource, and the opinions of authors and other contributors are their own and should not be taken as financial advice. If you require advice. HODL FM strongly recommends contacting a qualified industry professional.