Stablecoins are poised to change the banking, potentially drawing $1 trillion in deposits away from traditional banks by 2028.

Dollar-pegged tokens offer households and businesses easy access to USD outside conventional financial systems, a trend that could accelerate despite regulatory limits on interest payments.

Impact

In their report, Geoffrey Kendrick and Madhur Jha of Standard Chartered highlight that depositors in emerging markets often prioritize preserving capital over chasing higher yields. Even with the GENIUS Act restricting U.S.-compliant stablecoin issuers from offering direct interest, adoption is expected to grow rapidly.

Two-thirds of the existing stablecoin supply already functions as savings in emerging markets. Analysts estimate the global stablecoin market could reach $2 trillion by 2028, a benchmark cited by the U.S. Treasury in policy discussions.

Current stablecoin holdings in these regions total roughly $173 billion, with projections suggesting a surge to $1.22 trillion within three years.

This would account for about 2% of total deposits in vulnerable economies such as Egypt, Pakistan, Bangladesh, Sri Lanka, Turkey, India, and Kenya.

Observations

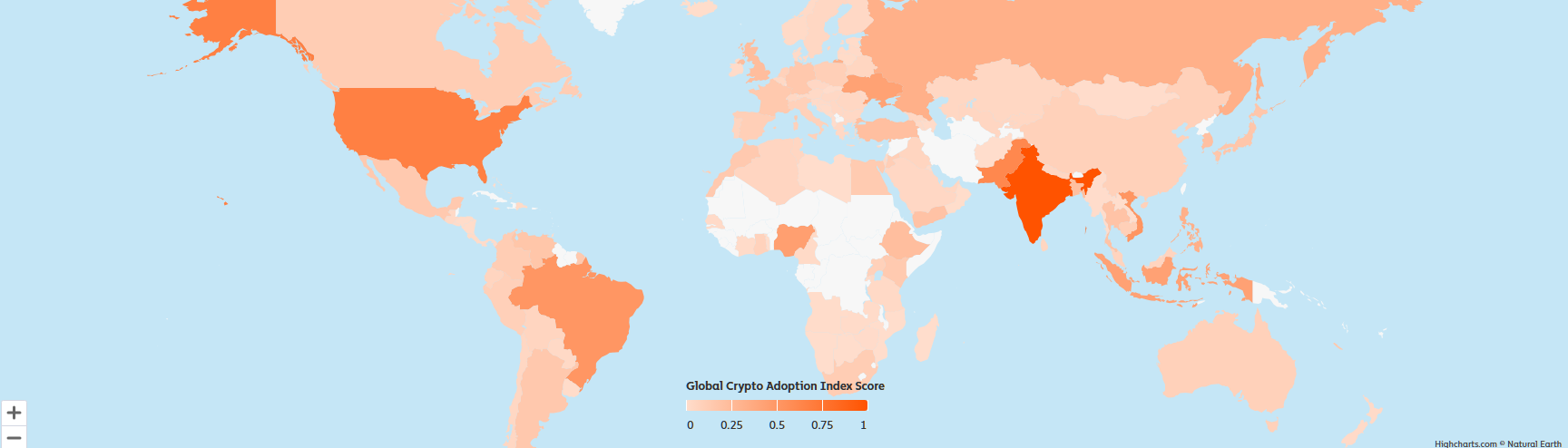

Fresh data from Chainalysis reinforces just how global the move toward stablecoins has become.

The 2025 Crypto Adoption Index shows that Asia-Pacific now leads worldwide growth in on-chain activity, with adoption climbing nearly 70% year over year. Emerging economies such as India, Pakistan, and Vietnam rank among the top nations for grassroots crypto use, driven largely by stablecoins as a practical hedge against inflation and currency volatility.

Transaction volumes in countries like Singapore and Hong Kong have surged, supported by platforms such as dtcpay and Grab. Hong Kong is also preparing a regulatory framework to integrate stablecoins into mainstream finance, signaling official support for the digital asset ecosystem.

Stablecoins like USDT and USDC dominate transaction volumes, each processing more than $1 trillion monthly, while smaller tokens such as PYUSD and DAI continue to gain traction.

Venezuela offers a clear example of this shift.

With annual inflation hovering between 200% and 300%, citizens increasingly rely on USDT and USDC. Merchants frequently denominate prices in stablecoins, locally dubbed “Binance dollars”, as the bolivar’s value continues to collapse. Chainalysis data ranks Venezuela 13th globally in crypto adoption, reporting a 110% usage growth in 2024 alone.

In 2023, cryptocurrency accounted for 9% of the $5.4 billion in remittances sent to the country, with small businesses and major retailers accepting stablecoins via various platforms. Brazil and Argentina are following similar patterns. According to Fireblocks, stablecoins now represent 60% of crypto transactions in both countries, reflecting growing business adoption as inflation erodes local currency purchasing power.

This global acceleration supports Standard Chartered’s forecast: as stablecoins grow more accessible and trusted, they could indeed pull massive deposits away from banks, redefining how emerging markets and eventually the world think about money.

Implications for banks

This migration toward stablecoins could pressure correspondent banking networks, payments systems, and foreign exchange revenue streams. Banks may offset some of these losses by offering custody services for stablecoin reserves or integrating digital assets into treasury and cross-border settlement operations.

Banks are exploring stablecoin solutions for treasury and payments, highlighting how traditional institutions are adapting to this shift.

The stablecoin market has already surpassed $300 billion in capitalization, led by Tether’s USDT and Circle’s USDC. To reach Standard Chartered’s $1 trillion projection in emerging markets by 2028, this growth trajectory will need to accelerate significantly.

Disclaimer: All materials on this site are for informational purposes only. None of the material should be interpreted as investment advice. Please note that despite the nature of much of the material created and hosted on this website, HODL FM is not a financial reference resource, and the opinions of authors and other contributors are their own and should not be taken as financial advice. If you require advice. HODL FM strongly recommends contacting a qualified industry professional.