The day that all crypto enthusiasts have been eagerly awaiting has arrived! The Securities and Exchange Commission (SEC) approved 19b-4 applications from VanEck, BlackRock, Fidelity, Grayscale, Franklin Templeton, ARK 21Shares, Invesco Galaxy, and Bitwise, greenlighting rule changes allowing the listing and trading of spot Ether ETFs on respective exchange platforms. This groundbreaking decision comes amidst rumors swirling around whether the securities regulator should label Ether as a security.

Related: Ethereum ETFs Filing Process Sees Abrupt Progress, Odds Jump Back to 75%

Though 19b-4 has been given the green light, ETF issuers still need the SEC to sign off on the corresponding S-1 registration statements for spot Ether ETFs to officially hit the trading floor. Experts suggest that this process may extend over days, weeks, or possibly even months.

Crypto commentator Zach Rynes and many others also note that while the ETFs have been approved, they haven’t yet received the go-ahead to launch. This requires an approved S-1 form, which is a comprehensive document encompassing detailed information about the firm’s financials, risk profile, and the securities they intend to offer.

VanEck has just submitted a revised S-1 application to the SEC.

Conditions for Expedited Approval from the SEC

Spot Market Oversight

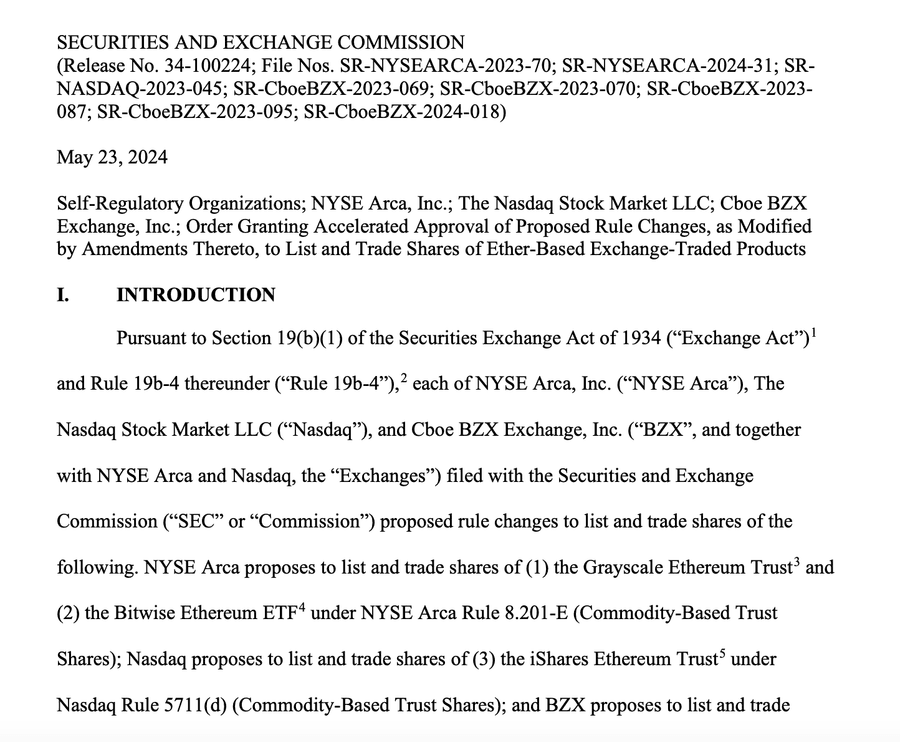

The Securities and Exchange Commission (SEC) has stressed the importance of entering into comprehensive joint surveillance agreements with the Chicago Mercantile Exchange (CME) to identify and prevent fraud and manipulation. Each exchange supports a comprehensive joint surveillance agreement with CME through its membership in the Intermarket Surveillance Group.

However, CME currently does not oversee spot Ether markets, raising concerns about effective oversight and the potential detection of fraud and manipulation. While spot Ethereums are not traded on CME, futures contracts are. Thus, the high correlation between the futures and spot markets means that price manipulation in the spot market is likely to affect the futures market.

In addition to the analysis provided by the applicants, the SEC has conducted its correlation analysis, examining data on CME Ether futures prices and spot trading pairs ETH/USD on platforms like Coinbase and Kraken.

The analysis results confirmed that CME’s Ether futures market consistently maintained a high correlation with this subset of the spot Ether market over the last 2.5 years.

Portfolio Transparency Protocol

ETPs must regularly disclose their portfolio assets, including the amount of Ether and any available cash or equivalents. This information typically needs to be updated daily and posted on the ETP’s website and other major financial information platforms.

Market Integrity Accord

Similarly to agreements with CME, exchanges must have data-sharing agreements to exchange information with other regulated markets, enhancing their ability to detect and deter fraudulent and manipulative practices. Additionally, exchanges need to specify the conditions under which they will halt trading.

Market Data Accessibility Standard

Having information on quotes and last sales for each ETP through a securities’ information processor; availability of intraday indicative values (IIV) and net asset values on each ETP’s website; and dissemination of IIV by major market data providers, updated every 15 seconds during regular trading hours.

Other Comments

In the SEC’s concluding segment, named “Other Comments,” they delved into further discussions among commentators on investor protection issues, environmental concerns, as well as volatility and risks.

The Securities and Exchange Commission scrutinized these potential benefits and challenges in a broader context and concluded that these proposals align with the Exchange Act’s requirements, including fraud prevention and mitigating manipulative practices.

More Info on ETFs:

- What Does Spot Bitcoin ETF Mean for Investors?

- Bitcoin Critically Fell After the ETF Approval. What’s Next?

The main focal point, which both the SEC and other regulatory bodies should concentrate on, is the impact of merging cryptocurrencies with traditional finance on the broader financial system as we know it. The gradual consolidation and introduction of a myriad of derivative assets could have a significant impact on the financial system — consequences that remain largely unstudied and unresolved.

Disclaimer: All materials on this site are for informational purposes only. None of the material should be interpreted as investment advice. Please note that despite the nature of much of the material created and hosted on this website, HODL FM is not a financial reference resource and the opinions of authors and other contributors are their own and should not be taken as financial advice. If you require advice of this sort, HODL FM strongly recommends contacting a qualified industry professional.