If you have a hundred dollars in your pocket, it remains that way, a hundred-dollar bill. Each bill will always have a value of $1.

Yet behind this simple analogy, lies a $136 billion question heightening debate between U.S. lawmakers and stablecoin issuance companies.

On February 12, the Security and Exchanges Commission (SEC) released a notice to Paxos alleging BUSD was an unregistered asset class. SEC made it clear that continued issuance would result in problems with financial regulators. Meanwhile, a section of regulators want legislation to treat stablecoin companies in much the same way as banks.

Hence raising doubts in the crypto community on whether the regulator views the stablecoin as a valuable asset.

Is a stablecoin a valuable asset?

The article aims to provide a close evaluation of Paxos’ fallout with the New York Department of Financial Services.

What is a stablecoin?

Stablecoins are digital currencies designed to maintain a stable value, typically pegged to a fiat currency like the USD. A factor that triggered the SEC’s decision against Paxos centres on a person acquiring a stablecoin with the expectation of profit. With this in mind, a regulator could term them securities due to the third aspect of the *Howey Test.

On the other hand, stablecoin issuers argue their coins are not securities because they are simply a form of digital currency, similar to Bitcoin or Ethereum. Another pro-crypto argument is that the coins are not investments. Rather, they are a means of exchange, and therefore not subject to SEC oversight.

However, the SEC is emphasizing a definite criterion for determining what is a security, and this criterion is likely to umbrella most digital assets.

According to this criterion, BUSD and a few other stablecoins qualify as securities by either being backed by assets or being subject to investor speculations. The regulator has gone on to express concerns about stablecoins’ potential to fuel terrorist financing or money laundering.

History of Stablecoins

Rapid volatility led to the creation of the first stablecoin in 2014, BitUSD. With frequent fluctuations, there is always a broader transaction problem when using crypto.

Therefore, blockchain developers saw a stablecoin pegged to the United States Dollar on a 1:1 ratio was going to solve this need.

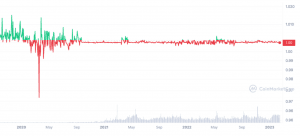

A stablecoin like the BUSD has maintained a stable value of approximately $1 since its inception. There could be other stablecoins in history that failed like TerraLuna’s UST.

It’s a nightmare right now with a price of nearly a few dollars cents. Even despite having been pegged to the dollar on a 1:1 ratio.

However, a few banks or traditional commodities have failed throughout history. The Washington Mutual Bank is a good example. JPMorgan had to write down billions of dollars in loans linked to the bank.

When a stablecoin breaks from its peg, holders have every right to seek legal action. Otherwise, there is no dignity in shutting the door for a good project that has maintained stability over the years. See the graph below by Coinmarketcap

Do stablecoins share similarities with money market funds and bank deposits?

Stablecoins are widely considered a new form of technology, however upon closer inspection of the definition above, one will note the term could as well denote money market funds and bank deposits.

Therefore, the debate is not just about the $136 billion market cap stablecoins on the blockchain. This may come as a shock to both those familiar with cryptocurrency and traditional financial services, but the truth is that stablecoins are not a recent development. Especially, if the above definition is anything to go by.

Fiat-backed stablecoins have the same fundamental structure as traditional financial instruments. Having a blockchain-based ledger provides the only distinction for digital stablecoins. It seems the SEC is preying on the $22.8 trillion combined market cap for both money market funds and bank deposits.

The stablecoin’s legal approach

A lawyer said that, while designed to maintain stability, purchasers of stablecoins may potentially benefit from arbitrage, hedging and staking opportunities. For example, Money market funds offer investors principal protection by maintaining a $1 stable value. The fund managers manage to do this while still providing a competitive rate of return.

The United States has a robust regulatory framework in place to protect consumers from such financial products. For banking institutions, charters, capital requirements, risk weights and operational controls are mandated. Money market funds, stable value funds and various types of insurance products require specific holdings, liquidity and structural parameters to ensure consumer protection.

However, issuance companies are convinced that stablecoins are more secure and less prone to risk than traditional mutual funds.

Owing to the fact that stablecoin reserves are rarely leveraged out. Besides, the reserves consist of more reliable backing instruments than those in traditional banking. Hence, making them risk-averse and more reliable than money market funds or bank deposits.

Nonetheless, despite the low economic risk associated with stablecoins, federal regulators remain persuaded to go after stablecoins. The biggest motivation is to protect U.S. consumers from risky investment vehicles. However, doing so necessities that U.S. consumers go back to their low-yield bank deposits. A situation that most pro-bitcoiners find unfair.

Regulators might favour the centralized nature of banks. Primarily, centralized structures are easier to control than decentralized financial organizations. Stablecoins on the other hand are a big concern because of the government’s inability cannot control the blockchain. Notwithstanding, this technological advancement is likely to continue undeterred.

Meanwhile, stablecoins are an essential safeguard for investors searching for shelter from unstable markets, and restricting access to these would adversely impact countless people worldwide. On February 13, Paxos released a statement announcing it had halted the minting of new BUSD coins. In the releases, the platform said they were working in close coordination with the NYDFS.

Conclusion: Industry Impact

The U.S. Securities and Exchanges Commission has a really knowledgeable counsel behind it. The regulator’s inability to work with companies and provide sensible guidance is what perplexes many. A majority feel resorting to lawsuits is barbarian. Particularly for a nascent industry that has a lot of growing to do.

Several bills are in congress waiting to address clear regulations around stablecoins and cryptocurrencies. This provides a bright spot for stablecoins, as well as a double-edged sword if lawmakers fail to amend the Securities ACT.