Let’s get into this week’s crypto digest, where the ghosts of Mt. Gox return, NFTs face their reckoning, and regulators play their game of cat-and-mouse with Binance. Meanwhile, Congress debates the privacy implications of digital dollars. Buckle up; it’s a rollercoaster of tech, drama, and (decentralized) finance!

Déjà Vu with Mt. Gox & The Never-Ending Repayment Drama

Let’s kick off this week’s digest with a story as old as time – or at least as old as most of your crypto portfolios: the infamous Mt. Gox. You remember them, right? The crypto exchange that turned into a ghost ship, vanishing from our screens nearly a decade ago? Well, the show ain’t over just yet!

For those of you just tuning in, here’s a brief rewind. Mt. Gox, once the darling of the crypto world, suffered a minor hiccup (read: cataclysmic disaster) in 2014 when it somehow “misplaced” a staggering 850,000 BTC. And by “misplaced,” I mean they got hacked. Yes, that was a colossal whoopsy daisy worth billions in today’s dollars, affecting 24,000 of our fellow crypto comrades. Fast forward to 2022, and they’re talking “Restriction Reference Periods” and all sorts of fancy words. For the uninitiated, that’s essentially an elegant way of saying, “Hey, tell us what we owe you and maybe, just maybe, you’ll get your coins back at some point in time.”

But hold on, folks! The plot thickens.

Mt. Gox has recently taken center stage once more, announcing a change in the repayment deadline. The original D-day was slated for October 31, 2023. But in a twist that should surprise exactly no one, they’ve hit the snooze button on repayments. Now, creditors get to anxiously circle a new date on their calendars: October 31, 2024.

The reason for this shift? Well, apparently the Rehab Trustee (that’s Mt. Gox’s term for the folks handling the reparations) is struggling to “engage in discussions and share information” with banks and other entities involved in the repayments. They cited complications in sorting through necessary details with “banks, fund transfer service providers, and Designated Cryptocurrency Exchanges.” I mean, it’s only been almost 10 years – what’s the rush, right?

To their credit (pun intended), Mt. Gox claims that some lucky ducks, ahem, I mean “rehabilitation creditors,” who’ve done their homework and provided the required info might see some repayment by the year’s end. But when exactly? That’s as nebulous as the real identity of Satoshi Nakamoto. They’ve kept that detail closer to their chest than a whale clutching their private keys.

If you’re looking to hurl some inquiries their way, Mt. Gox generously offers an incredibly user unfriendly online “rehabilitation” portal. Just a heads up, they’re swamped with questions, so you’d be lucky to even get an answer by the time BTC hits its millionth block.

In conclusion, Mt. Gox’s repayment saga is a tragedy that just won’t end. And while the popcorn might be getting stale, one can’t help but keep watching. Stay tuned for the next dramatic update in… who knows, another decade? Happy HODLing, folks!

NFT Reality Check: From Market Meltdown to A Fresh Start in South Korea

Non-fungible tokens, popularly known as NFTs, once painted a dazzling picture for the world of crypto investors. In the 2021/22 bull run, NFTs witnessed an astounding trading volume, raking in nearly $2.8 billion in just August 2021. Their unique nature and integration with various forms of digital art and memorabilia ushered in a new era of digital ownership.

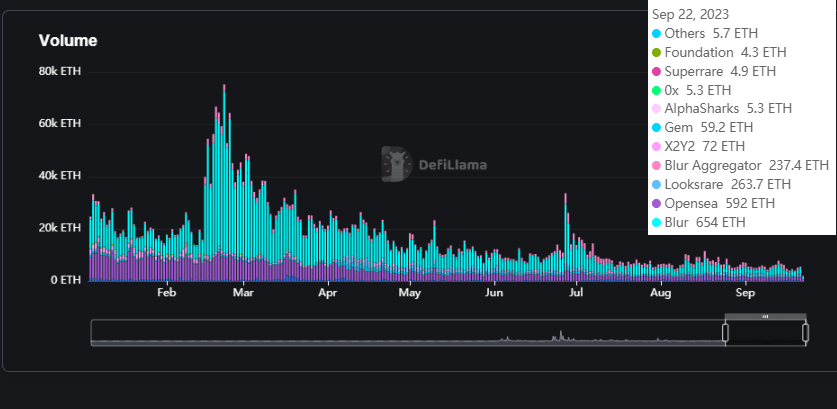

But the glitz and glamour of this digital asset didn’t last long. Fast-forward to July 2023, and the weekly traded value has nose-dived to just $80 million. Research from dappGambl shows that a shocking 95% of NFT collections now have a market cap of zero ETH, rendering them worthless. This tumble has left around 23 million people with unprofitable investments, but at least they can still enjoy their precious JPEGs as they bought them because they liked them right? Oversaturation and lack of demand for the growing number of NFT collections have played a key role in this downturn. For every success story in the NFT space, numerous other projects are struggling to find takers.

Currently, according to Defillama, the total volume of NFT’s being traded dropped to roughly 2000 ETH in the past day, which translates to give or take 3 million USD today.

Now, speaking of evolution, let’s take a look at South Korea. There’s a shimmering silver lining in the NFT dark clouds courtesy of Dreamus, the entertainment tycoon. They’re bringing a new beat to the NFT game by rolling out NFT tickets for K-Pop concerts, musicals, and more, all via SK Planet’s OK Cashbag loyalty rewards app. Leveraging the Avalanche blockchain, these blockchain tickets aim to tackle the bot-infested, scalper-ridden ticketing world. With NFTs, artists can disable resales or cap resale prices.

Adding to this, Ava Labs’ Justin Kim says that blockchain ticketing doesn’t just cut out scalpers but “improves the overall event experience.” These aren’t your typical OpenSea-variety NFTs though. They’re stealthy, visible only to buyers and activated on the event day itself.

Dreamus, an ally of big names like Psy and Twice, alongside SK Planet, plans to launch an NFT marketplace later this year. When asked about Korea’s crypto climate, Kim said, “There’s increasingly more adoption at both retail and business levels.”

In conclusion, while the broad NFT landscape seems frosty, there are pockets, especially in Korea, where the digital revolution is heating up. Only time will tell if NFT’s will actually find real world utility. Until then, happy collecting! 🎵🎨🎟️

Binance Claps Back: The SEC Suit & The Saga of Regulatory Whack-a-Mole

As the cryptocurrency world watched with bated breath, the latest episode in the “Crypto vs. Regulators” saga unfolded, featuring our main protagonists – Binance, its charismatic CEO Changpeng “CZ” Zhao, and the no-nonsense (or perhaps all-nonsense?) SEC.

In a move straight out of a courtroom drama, Binance and CZ jointly filed a motion to dismiss the SEC’s lawsuit against them, effectively telling the regulator, “You’re out of your depth here.” According to their spicy Sept. 21 filing, Binance and Zhao didn’t just plead innocence; they went on the offensive, claiming the SEC had overstepped its authority. The 60-page document might as well have been titled, “A Masterclass in Throwing Regulatory Shade.”

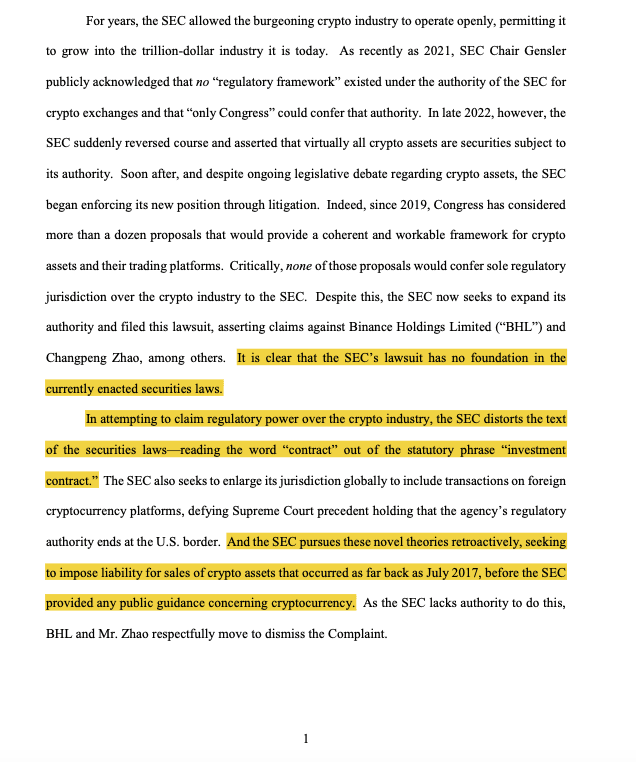

The filing took a jab at the SEC, highlighting its sudden U-turn in the crypto space. Remember the days when the SEC permitted the crypto industry to flourish? CZ sure does. As recently as 2021, SEC Chair Gensler acknowledged the absence of a “regulatory framework” for crypto exchanges under the SEC’s jurisdiction. But, in a plot twist reminiscent of a daytime soap opera, the SEC had a change of heart in 2022, suddenly deeming nearly all crypto assets as securities under its oversight.

But Binance and CZ weren’t going to take it lying down. They’ve clapped back, asserting that the SEC is basically making up the rules as they go, attempting to put a regulatory stranglehold on an industry they’ve previously allowed to flourish. With finesse and a touch of flair, Binance’s lawyers pointed out that the SEC is pulling some retroactive shenanigans, wanting to punish for actions from as far back as 2017. “Remember when you guys didn’t really know or care about crypto?” Binance’s motion seemed to jest, “Well, we do!”

Another golden nugget in this thrilling crypto drama? The allegation that the SEC was warping securities laws. The filing said, “In attempting to claim regulatory power over the crypto industry, the SEC distorts the text of the securities laws.” Ouch!

Alright….

This isn’t the first regulatory rodeo for Binance, though. Before the SEC came knocking, the CFTC also sued Binance, alleging it failed to register and violated guidelines. Since then, Binance.US has seen trading volumes plunge, and they’ve bid adieu to a significant chunk of their workforce.

Through the twists and turns, CZ remains steadfast, portraying the role of a CEO defending his empire against the regulatory dark arts. His message is clear: Binance is here to stay. Whether the SEC is the villain or misunderstood protector in this saga, only time will tell.

House Committee Thinks Twice About Going Full Digital

In a move that had cryptocurrency enthusiasts spitting out their morning coffee, the United States House Financial Services Committee took a bold stand against Central Bank Digital Currencies (CBDCs). Enter the “CBDC Anti-Surveillance State Act” which, despite its dramatic title, actually has some noble intentions at heart.

Tom Emmer, known in the political arena as the Majority Whip of the House, is championing this act. Emmer, who may even have a sixth sense for tech foresight, has concerns that are quite endearing. Picture this: a digital dollar system that respects the privacy of its users and doesn’t snoop into every digital transaction. Emmer’s stance? Let’s ensure our future digital buck doesn’t watch us more than our pet cats do when we’re trying to work from home.

But it’s not all rubber stamps and agreement nods in the House of Representatives. There’s still room for discussion, debate, and perhaps a spirited meme or two. This is democracy, after all!

Amidst this drama, the whirlwind romance (or perhaps more of a dramatic triangle) involving the US, the SEC, and the CFTC is making tech giants like Coinbase flirt with the idea of swiping right on other nations. Love and blockchain, always complicated, right?

Closing his act, Emmer took the stage to rally support for his bill, name-dropping the Chinese Communist Party and hinting that CBDCs might just be the next reality show’s surveillance cameras. With a cliffhanger awaiting the bill’s fate in Congress, we’re all on the edge of our seats, awaiting the next episode in this digital drama.

Conclusion

It’s evident that as the crypto frontier expands, both old specters and new regulators seek control of the narrative. From Mt. Gox’s endless dance to Binance’s battle for legitimacy, the push-pull dynamic reflects the industry’s growing pains. As we observe South Korea’s innovative strides and Congress’s hesitations, one must wonder: will the crypto world ever shake its Wild West reputation, or is this chaos the very essence of its allure?