This week in crypto: new DeFi initiatives aim to reduce global poverty, Kenya tests its first licensed framework amid Bitcoin ATMs, Bitfury launches a $1 billion tech fund, and Mastercard makes self-custody wallets easier with verified aliases.

First, let's check our top gainers and losers for this week.

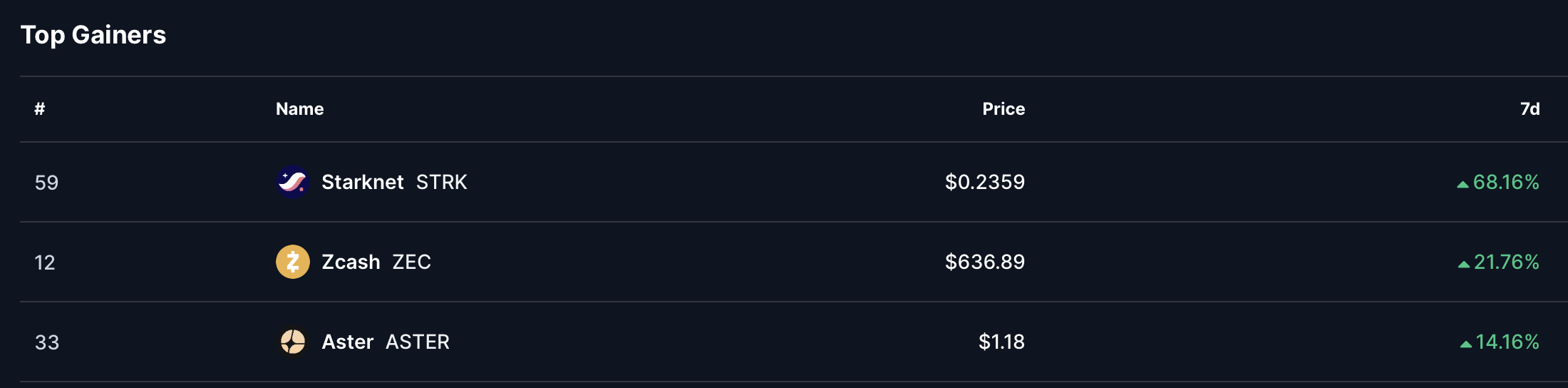

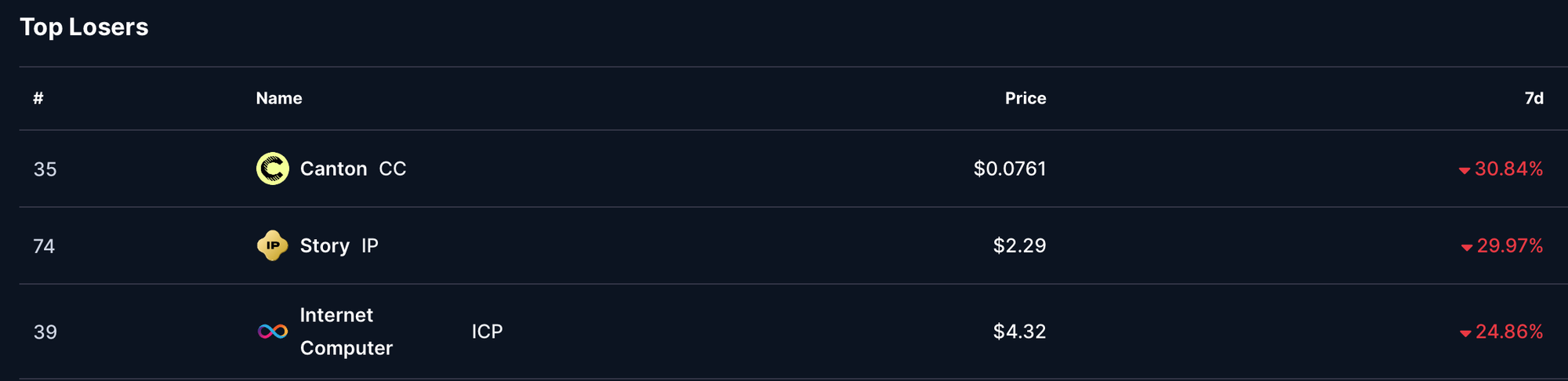

Top gainers and losers

- Starknet (STRK) - This week gained significant 68.16% to a total price of $0.2359

- Zcash (ZEC) - 21.76% rise to a total price of $636.89, good result this week

- Aster (ASTER) - Gained 14.16% and total price of $1.18

- Canton (CC) - Lost 30.84% this week to the end price of $0.0761

- Story (IP) - Drop of 29.97% with end price $2.29

- Internet Computer (ICP) - Loss of 24.86% and a total price of $4.32

Advocacy Group pushes DeFi as a tool against global poverty

A leading policy group in the crypto sector is promoting decentralized finance as a practical way to cut everyday financial costs for low-income and underserved communities.

In a new analysis, the DeFi Education Fund estimates that DeFi-based payment systems could save unbanked and underbanked individuals roughly $30 billion a year by lowering the fees typically charged for sending money across borders. The group points to familiar cases in which workers remit part of their wages to family members and lose a noticeable share to intermediaries.

It connects this dynamic to the “poverty premium,” the tendency for people with limited financial access to pay more for basic services.

According to the Fund, these higher costs stem from a traditional financial system built on multiple layers and outdated infrastructure, which makes serving low-balance customers expensive. By using automated, software-driven settlement, DeFi tools aim to lower that cost and give users more direct control over their transactions.

💡NEW BLOG: Why is the cost of U.S. financial services for lower-income families continuing to rise despite technological advances?

— DeFi Education Fund (@fund_defi) November 19, 2025

DEF's @jenn_rosenthal revisits a phrase coined in the early 2000s -- "the poverty premium" -- and explores the possibility of DeFi as a solution. pic.twitter.com/tScifp647x

The group also highlights domestic examples, such as the fees tied to cashing paychecks without a bank account or relying on money orders for routine payments, expenses that can accumulate quickly for households already under pressure. Public familiarity with decentralized finance remains low, but survey data cited in the report suggests that many Americans value the features commonly associated with it, including stronger control over funds, greater privacy around financial data, and a clear, continuous record of transaction history.

These arguments arrive as Congress works toward a federal market structure bill for digital assets. Committees in both chambers have released early drafts, though negotiations remain unresolved. Recent pushback from several Senate Democrats focused on how decentralized platforms should be treated under the law, highlighting ongoing divisions.

Despite delays caused by the recent government shutdown, Senate Banking Chair Tim Scott has indicated that lawmakers still aim to complete the legislation ahead of 2026.

Kenya’s new crypto law faces early test as Bitcoin ATMs appear in malls

Days after Kenya implemented its first comprehensive cryptocurrency law, Bitcoin ATMs have started appearing in major Nairobi shopping malls, challenging regulators who say no providers are yet licensed under the new framework. Local media reported machines branded “Bankless Bitcoin” installed alongside traditional banking kiosks, offering cash-to-crypto services to shoppers.

While Kenya has seen Bitcoin ATMs before, BitClub installed a few in 2018, adoption remained limited, and the devices never reached mainstream retail spaces.

CoinATMradar currently lists only two ATMs in the country.

The appearance of these machines coincides with the rollout of Kenya’s Virtual Assets Service Providers (VASP) Act of 2025, which establishes licensing for exchanges, custodians, wallet operators, and other crypto platforms.

Oversight is split: the Central Bank of Kenya (CBK) monitors payment and custody functions, while the Capital Markets Authority (CMA) regulates trading and investment activities.

Public Notice on the Virtual Assets Service Providers Act 2025 pic.twitter.com/suDoXIVWhN

— Central Bank of Kenya (@CBKKenya) November 18, 2025

Despite the law’s enactment on Nov. 4, the regulations needed to start licensing have not yet been issued. In a joint notice, CBK and CMA emphasized that no VASP is currently licensed to operate in or from Kenya, warning that any company claiming approval is doing so illegally. The National Treasury is developing regulations that will define the start of licensing.

The growing visibility of crypto infrastructure in upscale malls highlights a tension between regulation and adoption. Bitcoin has long circulated in informal channels, particularly in low-income areas such as Kibera, where residents use it as a practical alternative to traditional banking. AfriBit Africa co-founder Ronnie Mdawida noted that Bitcoin allows people to store value without formal documentation, offering a form of financial freedom for those living on limited incomes.

The situation underscores the challenges Kenya faces as it seeks to balance mainstream crypto adoption with regulatory oversight, while the market expands in both formal and informal sectors.

Bitfury launches $1 Billion fund to invest in ethical tech and crypto startups

Bitfury, one of the earliest Bitcoin miners since 2011, is shifting from mining to technology investment, announcing a $1 billion fund for AI and crypto startups. The company says the initiative will support ethical innovation, with funds drawn from prior operations, previous investments, and its network of investors. Deployment could begin as early as late 2025.

CEO Val Vavilov emphasized the company’s interest in projects that combine advanced computing with decentralized systems. Bitfury has experience in AI infrastructure, including its LiquidStack immersion-cooling solution for data centers, and its involvement with chip company Axelera AI.

The company is also exploring cryptography-based identity solutions that give individuals greater control over their personal data.

Today we announce our pivot to an investment firm with the launch of our $1 billion funding initiative for ethical innovation. https://t.co/iyKnD10wjV

— The Bitfury Group (@BitfuryGroup) November 18, 2025

Bitfury Announcement

Rising operational costs and mining difficulty have prompted many Bitcoin miners to scale back production or explore new business lines. Bitfury’s pivot reflects these challenges, as the sector faces tighter profit margins amid a fluctuating market.

Publicly traded miners have seen declines in recent months, highlighting the financial pressures on traditional Bitcoin mining operations.

The fund signals Bitfury’s intention to leverage its technical expertise beyond mining, focusing on projects that integrate emerging technologies with decentralized frameworks while maintaining an ethical approach to innovation.

Mastercard introduces user-friendly crypto aliases with polygon support

Mastercard is expanding its Crypto Credential program to self-custody wallets, enabling users to send and receive cryptocurrencies using simple, verified aliases instead of long wallet addresses. Polygon will provide onchain support, while payments firm Mercuryo handles identity verification and issues the aliases.

The system allows users to link a human-readable name to their wallet or request a soulbound token on Polygon to confirm ownership. Mastercard says the initiative is designed to reduce errors from copying complex addresses and make self-custody transfers more intuitive, aligning them closer to traditional payment experiences.

“By streamlining wallet addresses and adding meaningful verification, Mastercard Crypto Credential is building trust in digital token transfers,” said Raj Dhamodharan, Mastercard’s executive vice president of blockchain and digital assets.

Polygon CEO Marc Boiron added that the partnership simplifies self-custody and makes it more accessible for everyday users.

Big news:@Mastercard chooses Polygon to launch username-based transfers for self-custody wallets, with @mercuryo_io. pic.twitter.com/p0aTlP7wdp

— Polygon (@0xPolygon) November 18, 2025

Mastercard chooses Polygon to launch username-based crypto transfers

Mercuryo, the program’s first issuer, noted that the rollout reflects growing demand for secure, user-friendly crypto services that do not compromise wallet sovereignty.

This launch builds on Mastercard’s broader crypto strategy, which includes partnerships with Kraken for European debit cards, MetaMask for self-custody payments, and Chainlink to enable direct onchain crypto purchases for its three billion cardholders. The system integrates multiple Web3 partners, including Shift4 Payments, Swapper Finance, XSwap, and ZeroHash, the latter providing liquidity for fiat-to-crypto conversions.

Mastercard’s initiative aims to make digital asset transfers safer and more straightforward while maintaining users’ control over their wallets, marking a step toward more practical and widely adoptable crypto solutions.

Disclaimer: All materials on this site are for informational purposes only. None of the material should be interpreted as investment advice. Please note that despite the nature of much of the material created and hosted on this website, HODL FM is not a financial reference resource, and the opinions of authors and other contributors are their own and should not be taken as financial advice. If you require advice. HODL FM strongly recommends contacting a qualified industry professional.