Tether and Circle still dominate inflows, but rising challengers and bank-backed tokens hint at a changed landscape.

For nearly a decade, Tether’s USDT and Circle’s USDC have towered over the stablecoin sector, commanding what many saw as an unshakable duopoly.

But the numbers are shifting.

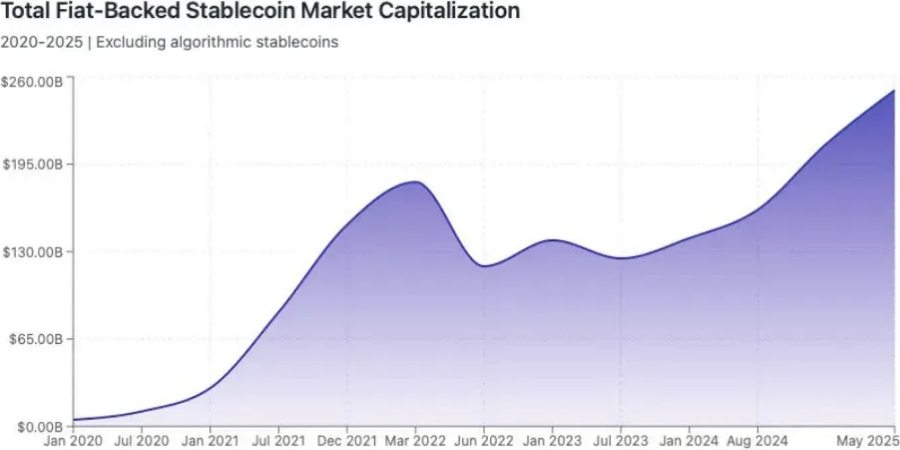

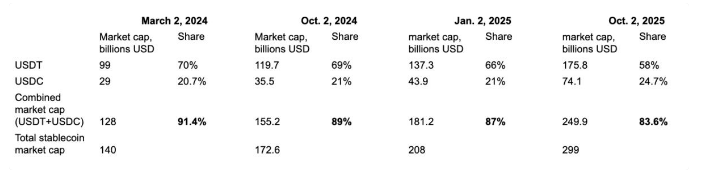

The two giants, long considered untouchable, have lost more than five percentage points of market share since October 2024, sliding from 89% to just 83.6% today, according to DefiLlama.

Industry analyst Nic Carter of Castle Island Ventures has called the moment plainly:

“The stablecoin duopoly is ending.”

USDT & USDC at their peak

It wasn’t long ago that USDT and USDC appeared unstoppable.

In March 2024, when the stablecoin market hovered around $140 billion, Tether accounted for $99 billion in circulation while Circle held $29 billion, together a record 91.6% share.

That dominance has eroded, despite both tokens actually growing in supply. The slip comes not from contraction but from competition.

“It has fallen to 86% since its peak last year, and I believe it will keep falling,”

Carter said on X, pointing to new regulatory dynamics, aggressive intermediaries, and a “race to the bottom” in yield. The pressure is coming from new entrants like Sky’s USDS, PayPal’s PYUSD, and World Liberty’s USD1.

But the biggest story of 2025 is Ethena’s USDe.

By passing yield from the crypto basis trade back to holders, USDe has surged to a $14.7 billion supply in less than a year, making it the most disruptive stablecoin since Tether itself.

Carter expects more startups to follow, “undercutting major issuers on yield” and reshaping what users expect from holding a dollar-pegged token. Even Circle, he noted, has quietly been working with Coinbase on yield-bearing versions of USDC.

Banks enter the arena

Traditional banks are circling the stablecoin market too.

JPMorgan and Citigroup are exploring consortia-issued tokens, while a coalition of European banks led by ING and UniCredit announced plans for a euro-denominated coin to be launched under the EU’s MiCA regime by 2026.

“No bank individually has the ability to create the necessary distribution to rival Tether,” Carter argued. “But together, bank consortia make by far the most sense.”

The road ahead

The stablecoin market has grown too large for any single issuer to dominate uncontested.

As yields, regulation, and institutional adoption reshape the terrain, Tether and Circle may remain leaders, but not monopolists. Carter’s reference to “new regulatory dynamics post-GENIUS” points to the Trump-era GENIUS Act, which is designed to lock in dollar-backed supremacy in stablecoins.

In practice, the GENIUS Act could accelerate the very fragmentation: raising barriers for smaller players while nudging banks and big institutions to step into the stablecoin race. But for now, USDT and USDC still dominate inflows and global liquidity. Yet the cracks are visible, and history suggests once challengers get momentum, the cycle is hard to reverse.

The duopoly, it seems, may be ending, not with collapse, but with competition.

Disclaimer: All materials on this site are for informational purposes only. None of the material should be interpreted as investment advice. Please note that despite the nature of much of the material created and hosted on this website, HODL FM is not a financial reference resource, and the opinions of authors and other contributors are their own and should not be taken as financial advice. If you require advice. HODL FM strongly recommends contacting a qualified industry professional.